STRC Discount Widens as Leverage Wipeouts Accelerate Decline

Bitcoin has fallen roughly 50% since Michael Saylor’s Strategy launched Stretch (STRC), its flagship Bitcoin-funding vehicle, in late July 2025. The decline has pushed STRC to trade at a 13% discount to its $100 par value, slowing the company’s Bitcoin acquisition pace as margin liquidations accelerate the sell-off.

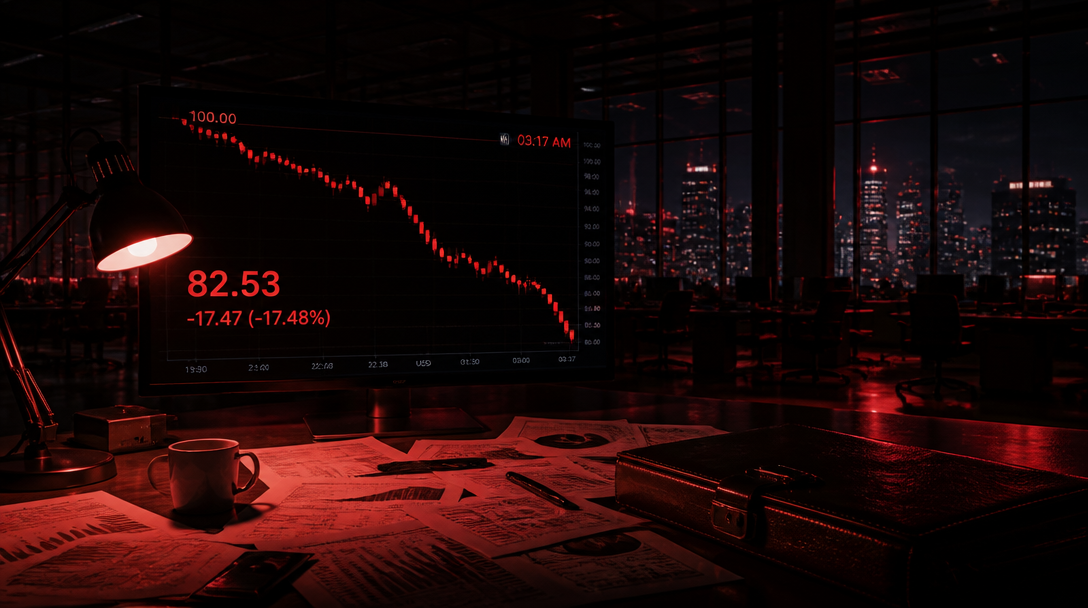

On Thursday, June 19, STRC hit a record low of $82.53 before closing at $88.59. The widening discount has contributed to a pause in at-the-market share issuance, a key mechanism Strategy relied on to fund Bitcoin purchases without diluting shareholders.

Strategy’s Bitcoin treasury now holds more than 846,000 BTC. In April 2026, the company bought 34,164 BTC for $2.54 billion in a single week. May saw Strategy add 24,869 BTC for roughly $2.01 billion. But the pace has slowed sharply. In the week ending June 8, Strategy purchased only 1,550 BTC for $101 million. The following week, ending June 15, Strategy added 1,587 BTC for $100 million. In June, Strategy also sold 32 BTC for about $2.5 million to cover dividend obligations.

STRC was designed to trade near par value through adjustable dividends, with proceeds used to acquire Bitcoin. The instrument’s dividend schedule was moved to semi-monthly payouts from monthly. The current annualized dividend rate stands at 11.5%, but the widening discount has lifted the effective yield to 13%. At discounted entry prices, yields climb further: 12.8% for buyers at $90, and 13.5% for buyers at $85.

The collapse has sparked debate over whether Saylor’s Bitcoin flywheel strategy remains viable. A flywheel in finance is a self-reinforcing business model where growth in one metric directly helps grow another. STRC’s original premise relied on the instrument trading near par, enabling continuous capital raises to fund Bitcoin acquisitions.

Jesse Myers, head of Bitcoin strategy at The Smarter Web Company, argued the sell-off reflects a leverage wipeout rather than fundamental deterioration. “Strategy is fine,” Myers said. Scott Melker, an analyst, echoed this view, noting that STRC offers attractive yields at discounted prices.

Critics contest this narrative. Peter Schiff, a longtime Bitcoin skeptic, called STRC “a classic centralized Ponzi.” DonAlt, a crypto trader, said the instrument was “trading like a Ponzi.” Both argue STRC operates as a scheme dependent on fresh capital raises to sustain dividend payments.

Strategy has not directly addressed Ponzi scheme allegations in recent statements. The company may announce its next dividend rate on June 30, 2026.

Under unchanged conditions, Strategy can pay STRC dividends for 32 years, assuming 2% annual Bitcoin appreciation. That calculation assumes no further price declines and continued access to capital markets. The pause in at-the-market issuance suggests both assumptions now face pressure.